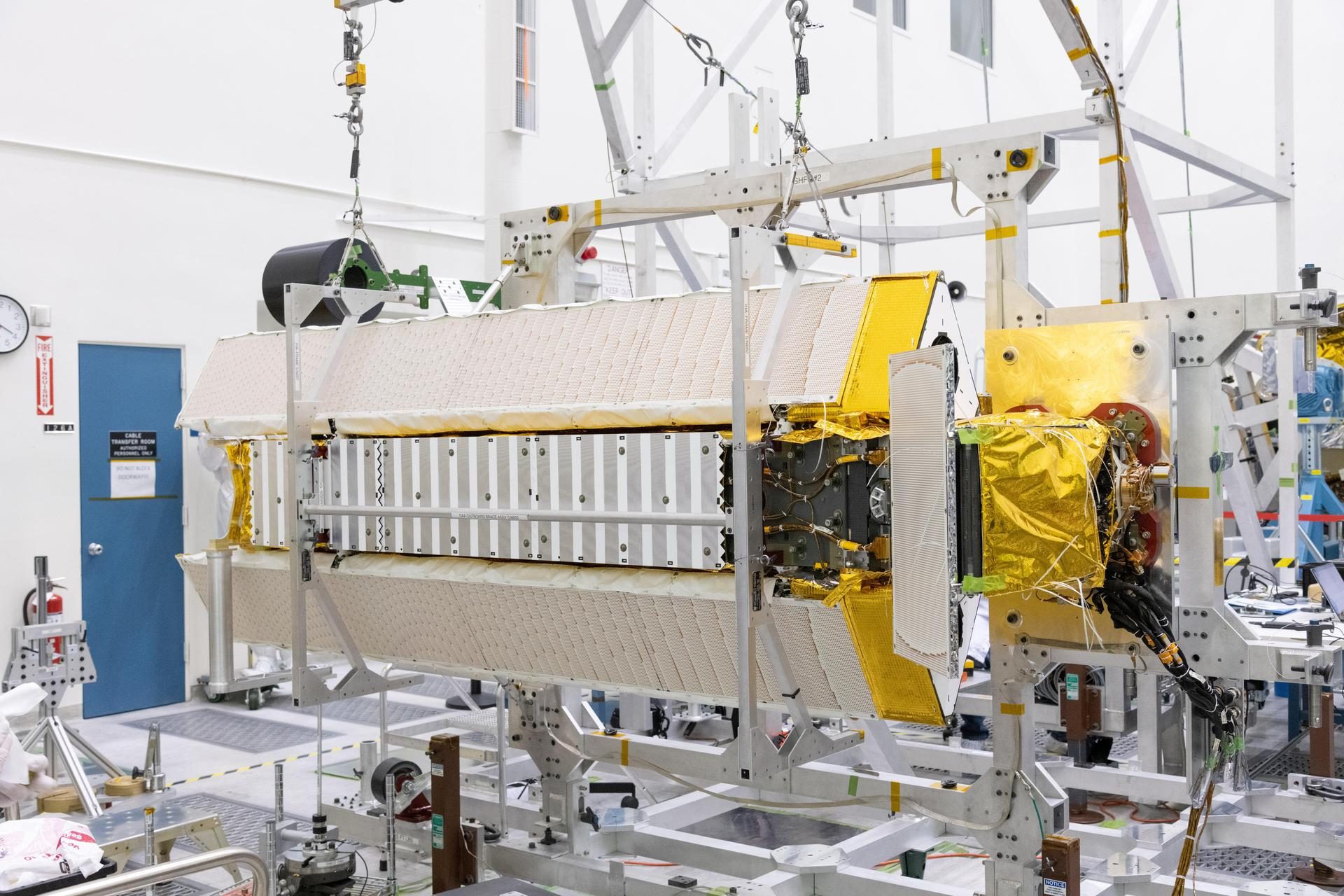

Spacecraft · clean-room integration

A comprehensive guide to commercial space assets, orbital infrastructure, and the $626 billion industry that is transforming how the world communicates, navigates, and observes our planet.

Sources: Novaspace Space Economy Report (Jan 2026), Space Foundation, MarketsandMarkets

Satellites operate at different altitudes depending on their mission. Altitude determines everything: coverage area, signal delay, lifespan, cost, and the number of satellites needed to deliver a service.

| Characteristic | LEO — Low Earth Orbit | MEO — Medium Earth Orbit | GEO — Geostationary Orbit |

|---|---|---|---|

| Altitude | 200 – 2,000 km | 2,000 – 35,786 km | 35,786 km (fixed) |

| Orbital period | ~90 minutes | 6 – 12 hours | 24 hours (matches Earth) |

| Signal latency | ~4 – 20 ms (very low) | ~80 – 125 ms | ~600 ms (noticeable delay) |

| Coverage per satellite | Small footprint — needs large constellation | Medium footprint — 6–20 sats for global | ⅓ of the planet — 3 sats for near-global |

| Typical lifespan | 5 – 7 years | 10 – 15 years | 15 – 20 years |

| Unit cost | $0.25 – 1M per smallsat; $5–50M for large | $50 – 200M | $150 – 500M+ |

| Primary uses | Broadband (Starlink, OneWeb), Earth observation, IoT | Navigation (GPS, Galileo, GLONASS), broadband (O3b) | Broadcast TV, weather, fixed comms, military |

| Key operators | SpaceX, OneWeb, Planet Labs, Spire | SES (O3b mPOWER), GPS/Galileo | SES, Intelsat, Eutelsat, Viasat |

Why this matters for finance: Orbital altitude directly determines asset lifespan, replacement cycle, and capital intensity. GEO satellites behave like long-life infrastructure assets similar to wide-body aircraft. LEO constellations are more like fleets of narrow-body jets — shorter lives, higher volume, rapid refresh cycles. Each demands a different financing approach.

The space economy produces a growing range of long-lived, revenue-generating physical assets. Each asset class has a different finance readiness profile based on asset life, revenue visibility, transferability, insurance, and legal framework maturity.

The workhorse of the space economy. Large, powerful satellites parked in geostationary orbit providing broadcast TV, fixed data services, and government communications. Think of them as the "wide-body aircraft" of space.

| Typical cost | $150M – $500M+ (build + launch) |

| Design life | 15 – 20 years |

| Revenue model | Transponder lease / capacity contracts |

| Contract terms | 3 – 15 years, often with renewal |

| Operators | SES, Intelsat, Eutelsat, Viasat, Arabsat |

| Manufacturers | Airbus, Thales, Boeing, Lockheed Martin, Maxar |

| Finance readiness | High — 15–20 yr lives, contracted capacity revenue, established insurance market, Berlin Space Protocol emerging |

Mega-constellations of hundreds or thousands of small satellites providing global broadband internet. Starlink alone operates ~10,000 active units. Fleet economics rather than single-asset finance.

| Typical cost per unit | $0.5M – $5M (mass production) |

| Constellation cost | $5B – $20B+ for full deployment |

| Design life | 5 – 7 years (continuous replacement) |

| Revenue model | Consumer/enterprise subscriptions |

| Operators | SpaceX (Starlink), OneWeb, Amazon (Kuiper) |

| Finance angle | Fleet financing, sale-leaseback potential |

| Finance readiness | Moderate — 5–7 yr lives, fleet-level financing needed, subscription revenue less predictable, mass production reduces per-unit risk |

Imaging satellites capturing optical, radar (SAR), or multispectral data of the Earth's surface. Revenue comes from selling imagery and analytics — not bandwidth. Growing defence, insurance, and agriculture demand.

| Typical cost | $10M – $300M depending on resolution |

| Design life | 5 – 10 years |

| Revenue model | Data subscriptions, government contracts |

| Operators | Planet Labs, Maxar, ICEYE, Airbus |

| Key customers | Defence, agriculture, insurance, mining |

| Finance angle | Recurring SaaS-like data revenue underpins debt |

| Finance readiness | Moderate–High — 5–10 yr lives, recurring data/analytics revenue, growing defence and commercial demand, diversified customer base |

Why ground matters: Every byte of satellite data must pass through ground infrastructure. The ground segment market was valued at $41 billion in 2025 and is growing at 15%+ CAGR. Ground stations are physical, fixed assets — often on long-term land leases — with 20+ year useful lives. They are among the most immediately "bankable" space assets.

High-throughput ground terminals connecting satellite broadband constellations to the internet backbone. Every constellation needs dozens of gateways. Physical assets — antennas, radomes, RF chains, buildings — on fixed sites.

| Typical cost | $5M – $30M per site |

| Useful life | 20 – 30 years |

| Revenue model | Capacity fees, hosting agreements, GsaaS |

| Operators | KSAT, RBC Signals, AWS Ground Station, Leaf Space |

| Demand driver | Every LEO constellation needs 40–100+ gateways |

| Finance angle | Long-life, fixed-location — very similar to telecom towers |

| Finance readiness | Very High — terrestrial assets, 20–30 yr lives, contracted revenues, standard insurance, no novel legal framework required |

Commercial facilities aggregating satellite traffic and connecting it to terrestrial fibre. They serve as hubs for content distribution, broadband backhaul, and enterprise services. Typically co-located with multiple operators.

| Typical cost | $10M – $50M per facility |

| Useful life | 20 – 30+ years (upgradeable) |

| Revenue model | Multi-tenant hosting, co-location fees |

| Operators | SES Techcom, Telespazio, Globecomm |

| Finance angle | Analogous to data centres — proven financing models |

| Finance readiness | Very High — multi-tenant revenue, long useful lives, upgradeable, proven data centre financing models apply directly |

Telemetry, Tracking & Command stations monitor satellite health, orbital position, and performance. They enable operators to control assets in real time. Without TT&C, a satellite is uncontrollable — making these stations essential infrastructure.

| Typical cost | $2M – $15M per site |

| Useful life | 20+ years |

| Revenue model | Managed service contracts, per-pass fees |

| Key point | Control of TT&C = constructive possession of satellite |

| Finance angle | Essential for creditor security — Berlin Space Protocol enables registration of rights |

| Finance readiness | Very High — mission-critical infrastructure, 20+ yr lives, managed service contracts, key element of creditor security package |

Reusable rockets are becoming long-lived capital assets. SpaceX's Falcon 9 boosters have flown 20+ times each. As reusability matures, launch vehicles may become financeable assets akin to commercial aircraft.

| Cost to build | $30M – $300M+ per vehicle |

| Reuse potential | 20+ flights per booster (Falcon 9 proven) |

| Revenue model | Per-launch fees ($60M – $150M/flight) |

| Key operators | SpaceX, Rocket Lab, Arianespace, ULA |

| Finance angle | Early stage — needs deeper secondary market and valuation frameworks |

| Finance readiness | Early Stage — reusable rockets becoming long-lived assets but no secondary market or valuation precedent yet |

Spacecraft that dock with existing satellites to refuel, repair, reposition, or extend their lives. Northrop Grumman's MEV has already extended GEO satellite life by 5+ years. This changes the residual value equation entirely.

| Typical cost | $50M – $200M per servicing vehicle |

| Value proposition | Extends a $300M satellite's life by 5+ years |

| Operators | Northrop Grumman (MEV), Astroscale, Orbit Fab |

| Finance angle | Impacts satellite residual values and depreciation assumptions |

| Finance readiness | Early Stage — limited insurance and valuation precedent, but proven commercial deployments (Northrop MEV) are building the case |

With the ISS scheduled for decommissioning by ~2030, commercial replacements are under development. These will serve as orbital platforms for research, manufacturing, tourism, and national laboratories.

| Estimated cost | $1B – $3B+ per station |

| Expected lifespan | 15 – 20+ years |

| Developers | Vast (Haven-1), Axiom Space, Blue Origin (Orbital Reef) |

| Revenue model | Government anchor tenancy + commercial services |

| Finance angle | Largest single-asset space financing opportunities |

| Finance readiness | Early Stage — $1B+ single assets with concentrated risk, but government anchor tenancy (NASA) de-risks; financing frameworks emerging |

Every satellite — whether a 50 kg LEO smallsat or a 6-tonne GEO spacecraft — is built from the same core subsystems. Understanding these is essential for assessing asset value and risk.

Generate electricity from sunlight and store it in batteries for eclipse periods. Power capacity determines what the satellite can do — more power means more transponders or higher-resolution sensors. Degradation of solar cells over time is a key factor in end-of-life planning.

The structural chassis housing propulsion, thermal control, attitude control, and avionics. Think of it as the airframe of the satellite. The bus is often a standardised platform (e.g., Airbus Eurostar, Thales Spacebus) onto which different payloads are mounted — a key enabler for redeployment.

The mission equipment — the reason the satellite exists. For communications satellites: transponders and antennas. For EO: cameras, SAR radar, or multispectral sensors. The payload is the primary revenue-generating component and drives the satellite's market value.

Transmit and receive data between the satellite and ground stations. Includes high-gain antennas for mission data, omnidirectional antennas for TT&C, and increasingly inter-satellite links (ISLs) for mesh networking between constellation members.

Chemical or electric thrusters for orbit raising, station-keeping, and end-of-life deorbiting. Electric propulsion (ion/Hall-effect) is now standard for GEO, offering lower mass but slower manoeuvring. Fuel reserves directly determine remaining useful life.

Manages extreme temperature swings — from +150°C in sunlight to -170°C in shadow. Uses radiators, heaters, heat pipes, and multi-layer insulation. Thermal system integrity is critical for long-term reliability.

The finance takeaway: A satellite's value is primarily in its payload and remaining fuel. The bus is a commodity platform. When assessing a satellite for financing, the key questions are: how much capacity does the payload have, what condition are the solar arrays in, and how much propellant remains? These determine remaining useful life and therefore economic value.

The space segment only works because of the ground infrastructure that supports it. Ground stations, teleports, and gateways form the critical physical link between satellites and end users — and they represent some of the most immediately financeable assets in the space economy.

| Ground Asset Type | What It Does | Typical Capex | Useful Life | Revenue Model | Closest Traditional Analogy |

|---|---|---|---|---|---|

| Gateway Station | Connects satellite constellation to internet backbone | $5 – 30M | 20 – 30 yrs | Throughput / capacity fees | Cell tower / fibre PoP |

| TT&C Facility | Commands, monitors, and controls satellites | $2 – 15M | 20+ yrs | Managed service / per-pass | Air traffic control facility |

| Teleport | Aggregates traffic, connects to terrestrial networks | $10 – 50M | 25+ yrs | Co-location, hosting, transit | Data centre / carrier hotel |

| Optical Ground Terminal | Laser-based high-bandwidth satellite downlink | $3 – 20M | 15 – 20 yrs | Capacity / per-session fees | Fibre landing station |

| Ground Station-as-a-Service (GSaaS) | Cloud-integrated, multi-mission ground access | Varies (capex-light) | N/A (service model) | Usage-based / subscription | Cloud hosting provider |

Ground is the entry point for space finance. Ground stations are terrestrial assets sitting on land, with 20+ year lives, contracted revenue streams, and known maintenance profiles. They require no novel legal frameworks to finance — existing infrastructure finance models apply directly. For an asset lessor, ground stations offer the lowest risk entry into the space economy while building the expertise and relationships needed for orbital asset transactions.

Space assets generate revenue through predictable, contracted services. The business model is built on long-term agreements providing recurring cash flows — exactly the kind of revenue profile that underpins asset finance.

Operators sell satellite capacity (measured in MHz or Gbps) under multi-year contracts to telecoms, broadcasters, governments, and enterprise customers. This is the dominant revenue model for GEO and MEO operators. Contracts often include escalation clauses and renewal options.

End-to-end satellite connectivity solutions for maritime, aviation, energy, and government customers. Operators provide the full stack — space segment, ground, terminals, and service management — under SLA-based contracts. Higher margins than raw capacity.

LEO mega-constellations sell direct-to-consumer internet subscriptions. Starlink reached 9M+ subscribers and generated an estimated $10B+ in revenue in 2025. Consumer churn is a risk, but scale creates powerful network economics.

Earth observation operators sell satellite imagery and derived analytics to agriculture, insurance, defence, mining, and environmental monitoring customers. Increasingly delivered as SaaS platforms. Recurring, diversified revenue.

Ground station operators charge per-pass fees, hosting agreements, or sell Ground-Station-as-a-Service (GSaaS) capacity. Multi-tenant teleports earn co-location revenue from multiple operators sharing the same facility. Predictable, utility-like cash flows.

Sovereign customers procure dedicated satellite capacity, hosted payloads, or bespoke ground services. These contracts carry strong counterparty credit (government-backed) and are often structured as availability-based payments — ideal for debt underwriting.

Aviation leasing proved that third-party ownership of high-value, long-lived transport assets creates more efficient markets. Over 50% of the world's commercial aircraft are now leased. Space assets share the same fundamental characteristics — but less than 5% are currently financed this way.

| Feature | Aviation Leasing | Space Asset Leasing |

|---|---|---|

| Market maturity | 50+ years, $300B+ market | Nascent — first major deals completed 2023–2025 |

| Asset registration | Cape Town Convention (CTC) | Berlin Space Protocol (not yet in force) |

| Repossession mechanism | Physical — fly aircraft to neutral jurisdiction | Constructive — transfer TT&C codes (ground-based) |

| Valuation infrastructure | ISTAT appraisers, blue book values | Emerging — no standardised residual value guides yet |

| Tax-efficient structures | Ireland S.110, JOL/JOLCO, ECA financing | Ireland S.110 applicable; JOLCO potential |

| Lessee credit quality | Airlines — cyclical, some weak credits | Sat operators — often investment grade or govt-backed |

| Lease penetration | ~50% of global fleet | <5% — massive structural opportunity |

The structural opportunity is clear. Space operators need capital to build and deploy assets. They increasingly prefer to keep capacity on their balance sheets rather than the hardware. Institutional investors need infrastructure-grade returns with long-duration cash flows. Asset-backed leasing connects these two pools — exactly as it did in aviation 40 years ago.

Caelum brings aviation-grade leasing expertise to the space sector. We provide sale-leaseback facilities and finance leases for satellites, ground stations, and orbital platforms — structured through Ireland's proven S.110 SPV framework.

Get in Touch