Latest Articles

What flexibility really buys you

Software-defined payloads break the single-tenant economics of a satellite. Why the Space Inspire and OneSat generation makes sale-leaseback credible in 2026 in a way it was not in 2010, and what the aviation airframe-versus-engines analogue looks like on orbit.

Caelum at SATELLITE 2026, Washington DC

Caelum Space Leasing was at SATELLITE 2026 (SATShow) in Washington, DC, meeting operators, manufacturers and capital partners from across the space economy.

SpaceX IPO: what it means for the commercial space economy

SpaceX's anticipated listing, most likely via a Starlink spin-off, would hand the sector its first daily-marked price for an orbital asset business. Reported figures run past $350bn. What a credible public benchmark actually changes for how the rest of the market is financed.

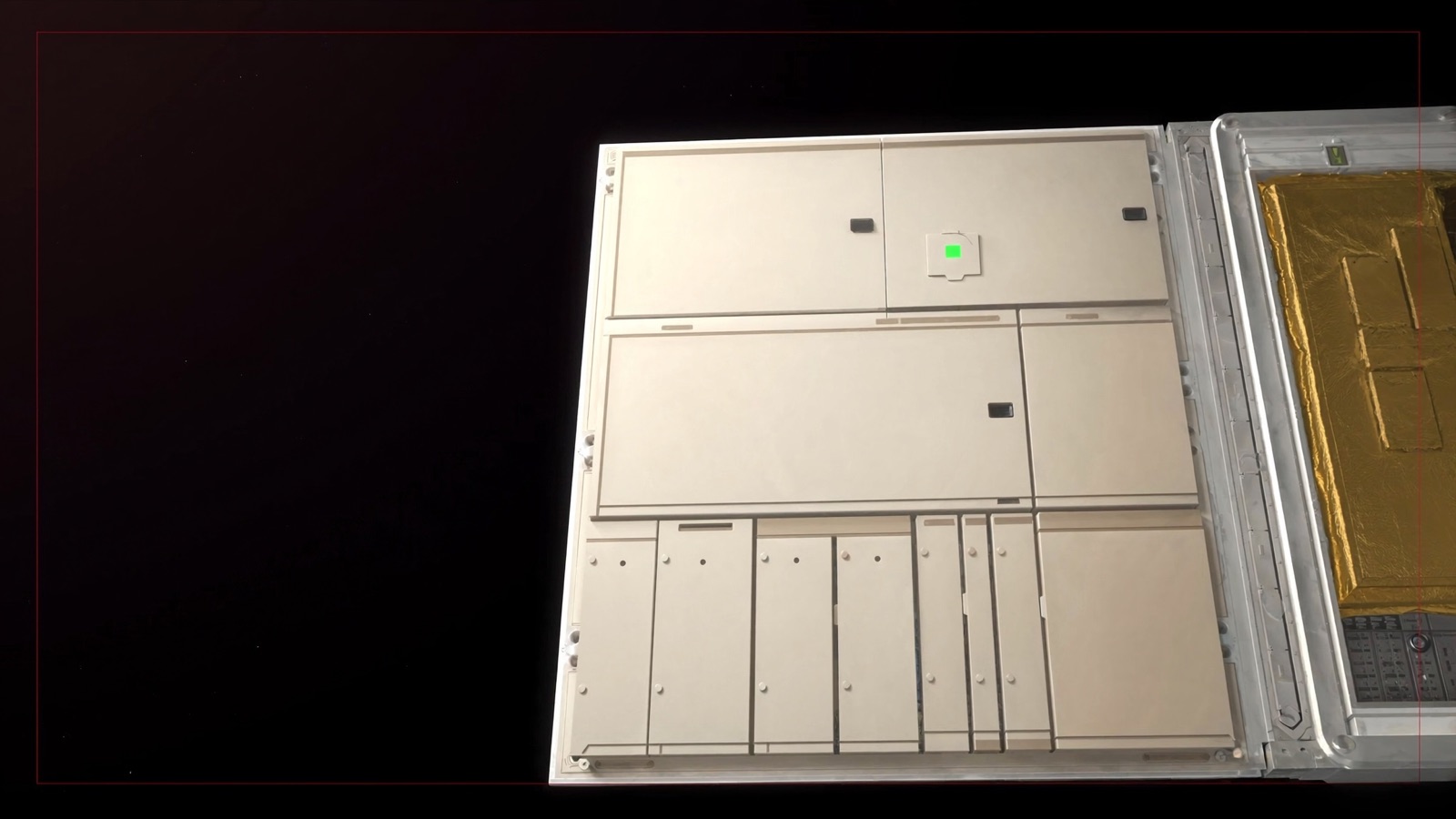

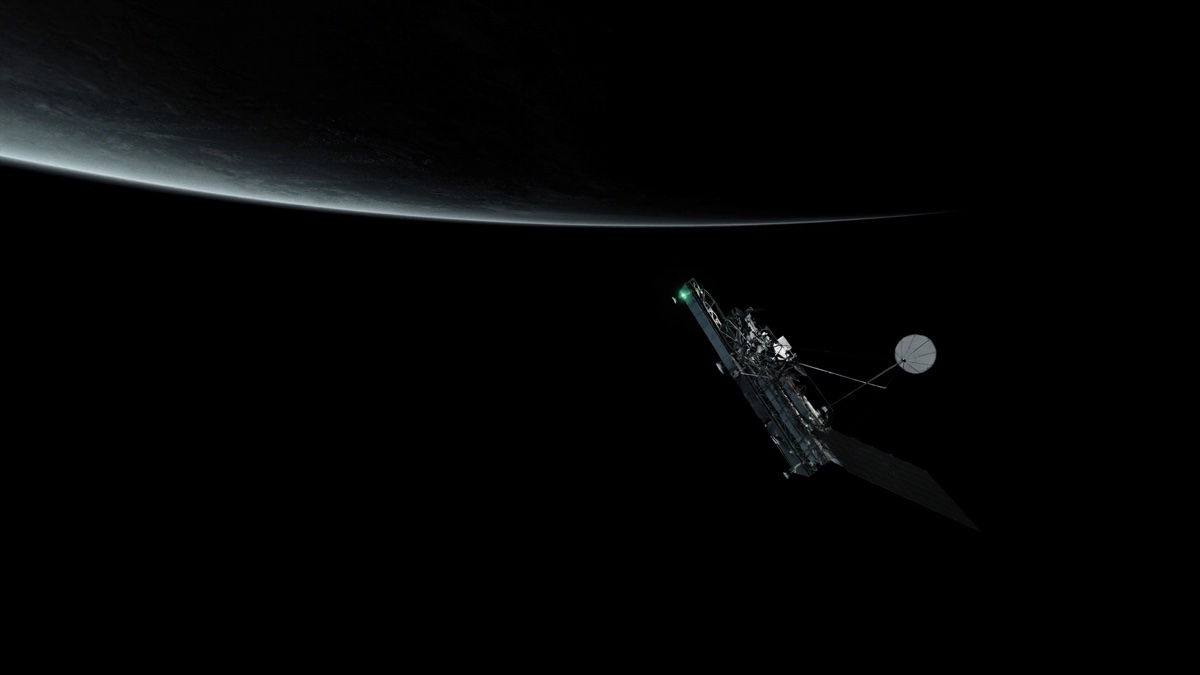

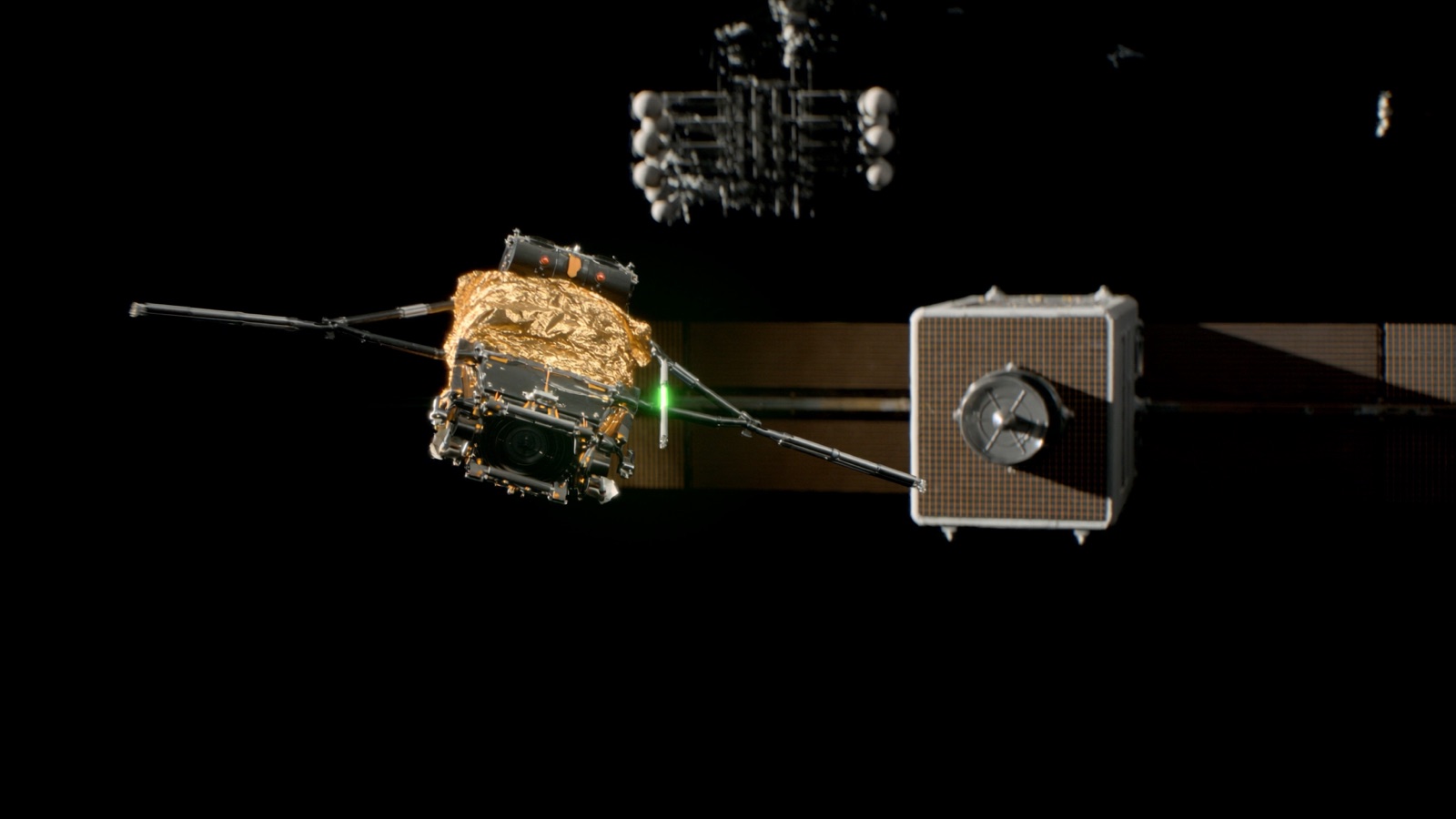

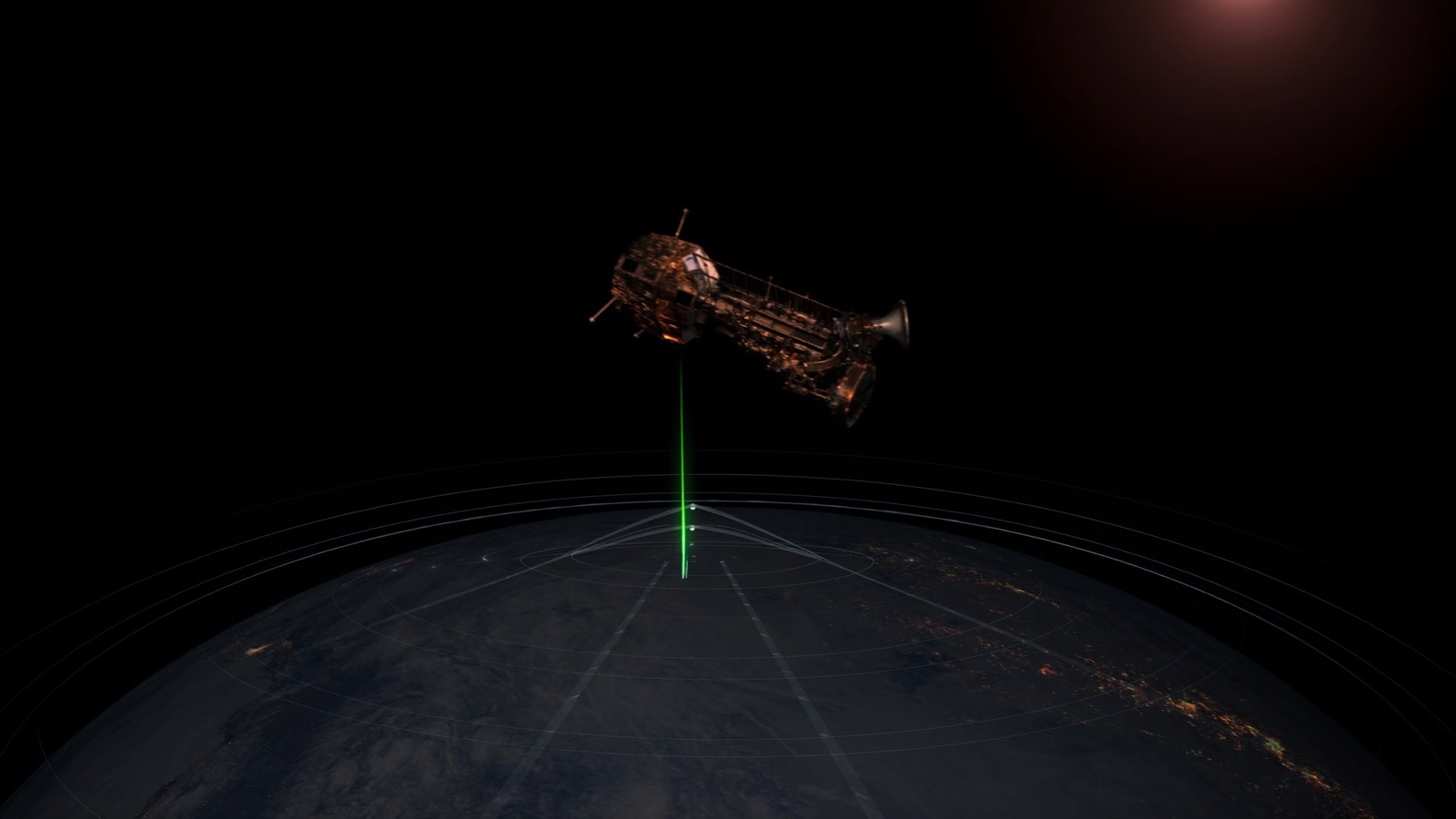

In-orbit servicing: the rise of satellite maintenance

Refuelling, life-extension and robotic inspection are turning fixed-lifespan satellites into maintainable infrastructure. What that does to useful-life, depreciation and end-of-lease assumptions, and why the aviation MRO analogue only holds for high-value GEO assets so far.

Caelum at Space-Comm Expo Europe, London

Caelum Space Leasing was at Space-Comm Expo Europe at ExCeL London, meeting operators, manufacturers and capital partners from across the European space industry.

The ground segment: why Earth-based space infrastructure matters

Satellites get the headlines; the dishes that talk to them get the contracted revenue. Why the ground segment, now shifting to a Ground Station as a Service model, is the cleaner leasing asset, and where Elfordstown and EU sovereignty fit Caelum's thesis.

Satellite spectrum: the most valuable real estate you can't see

Orbital slots and frequency rights are intangible assets that can outweigh the satellite they sit on. How the ITU filing regime, bringing-into-use rules and the C-band precedent shape repossession risk, residual value and what a lessor must diligence in any sale-leaseback.

From aviation to orbit: what aircraft leasing teaches us about space

The €350bn+ global aircraft-leasing market, much of it run from Dublin, is the working blueprint for space asset finance. Where the analogy maps cleanly onto orbit, where it breaks, and why an Irish Section 110 lessor is the natural home for it.

Space sustainability: debris, de-orbiting, and the business case

Orbital-debris rules are tightening from a 25-year guideline to five-year disposal mandates and a 2030 zero-debris target. Why end-of-life compliance is becoming a precondition for insurability, and therefore financeability, and why active debris removal is not yet bankable.