For most of the satellite era, a spacecraft was a fixed-life asset: launch it, run it until the propellant ran out, then write it off and let it drift into a graveyard orbit.

That assumption is starting to loosen. A small fleet of servicing vehicles is now operating in geostationary orbit, and the financial consequence matters more than the engineering novelty. If a satellite can be refuelled, relocated, inspected or have its station-keeping taken over by another vehicle, it stops being a depreciating block and starts to behave like maintainable infrastructure. That is a different underwriting problem.

What is actually flying

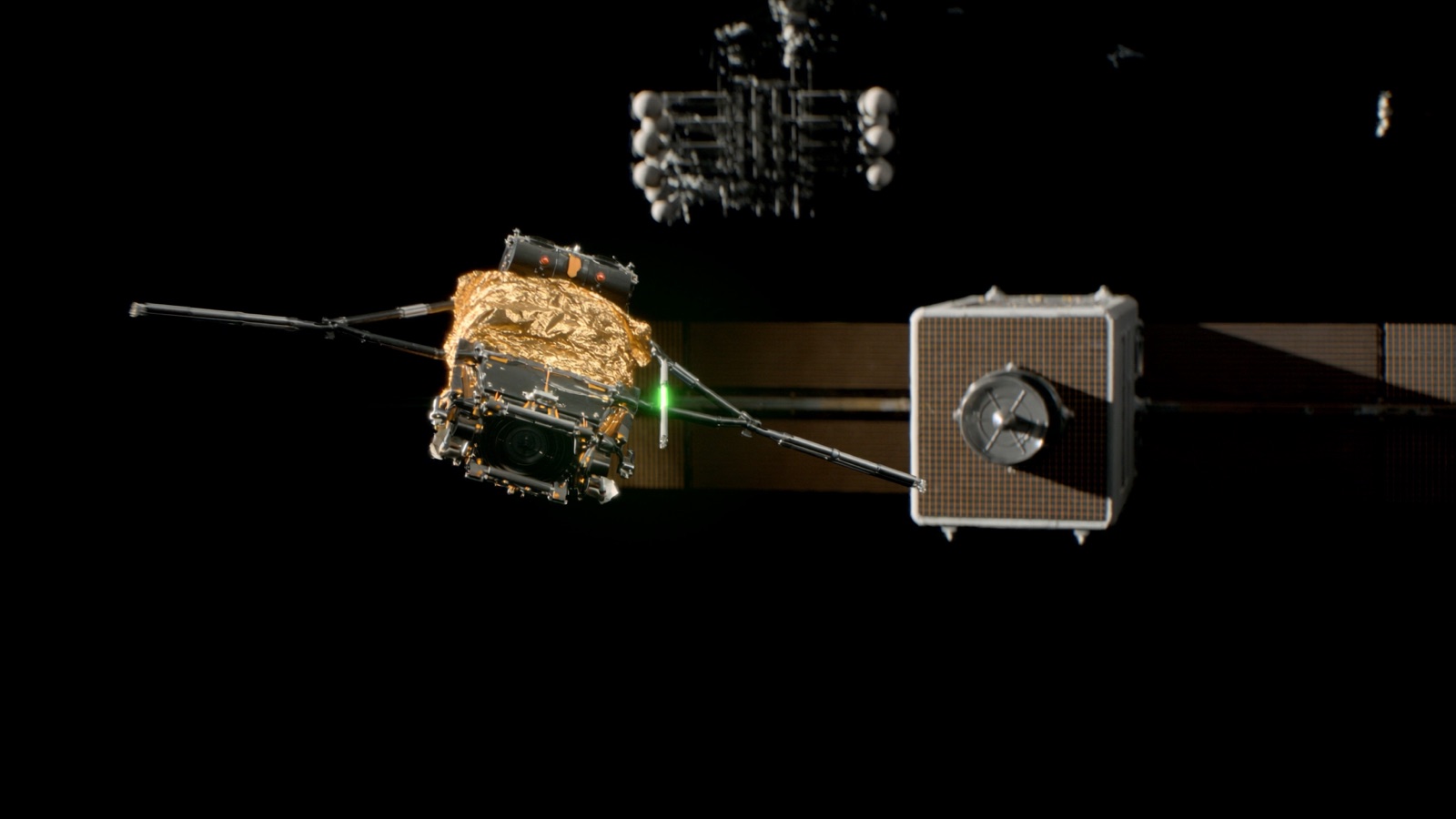

The clearest proof point is Northrop Grumman's SpaceLogistics business. Its first Mission Extension Vehicle, MEV-1, docked with Intelsat 901 in early 2020, took over station-keeping, and moved the satellite back into commercial service after it had nearly exhausted its fuel. MEV-2 followed in 2021, docking with Intelsat 10-02 while that satellite stayed live. Each MEV is contracted to provide roughly five years of life extension before relocating to its next client.

These are not refuelling missions. The MEV does not top up the host's tanks; it clamps on and supplies propulsion and attitude control using its own fuel, acting as a strap-on engine module. True refuelling, robotic component replacement and in-orbit assembly remain mostly at the demonstration stage. NASA's OSAM-1 programme aimed to refuel a satellite never designed to be serviced, before the agency wound it down in 2024 on cost grounds. Astroscale and ClearSpace are working the debris-removal and inspection side, the latter under an ESA contract. DARPA has run its own robotic-servicing work for GEO.

The honest summary: the capability is real but thin. It is concentrated in GEO, where assets are valuable enough to justify the cost, and most of the more ambitious functions have not yet flown commercially at scale.

The airframe and engines lens

Aviation finance has lived with the airframe / engines split for forty years. The lessor owns the airframe; the operator maintains the engines to contractual return conditions; hours-on-wing set what the asset is worth at redelivery. Servicing is the whole reason a 25-year-old narrowbody still has residual value.

Space hardware maps onto the same split, if imperfectly. The bus is the structural airframe, long-lived, expensive, the thing a lessor would rather own and keep. The consumables and the payload behave like the engines: their condition decides remaining useful life. Historically the space version had no MRO step. Once the propellant was gone, the airframe was gone too, regardless of how sound the structure was. In-orbit servicing is the missing maintenance event that lets the structure outlive its first tank of fuel.

Strip out servicing and an aircraft is also a fixed-life asset. The whole of aviation residual value rests on the assumption that the expensive parts get maintained. Space is only now acquiring that assumption.

What changes in the underwrite

For a lessor, three inputs move once servicing is credible for a given asset.

| Assumption | No servicing | With credible servicing |

|---|---|---|

| Useful life | Fixed by propellant load | Extendable in defined increments |

| Depreciation | Straight line to fuel exhaustion | Re-profiled around service events |

| End-of-lease condition | Effectively scrap | Returnable with documented life remaining |

The structure is familiar from engine MRO: you underwrite to a maintained condition, you hold the lessee to defined return conditions, and you price the residual on the basis that maintenance will happen. The difference is that a missed shop visit on a jet engine is recoverable, whereas a servicing failure 36,000 km up is not. The downside is harder and the supplier base is far narrower.

Where this is useful, and where it is not

Caution is warranted. Servicing only pencils out where the asset is worth far more than the mission, which today means high-value GEO satellites and a handful of government payloads. For a small LEO spacecraft built to be replaced cheaply, the economics point the other way: cheaper to deorbit and relaunch. Pricing in life extension for a sub-scale asset would be underwriting a capability that may never be procured.

For a lessor the practical move is modest. Treat servicing as optionality, not as base case. Where an asset is large, valuable and in an orbit a servicer can reach, a credible extension path supports a higher residual and a longer amortisation profile. Everywhere else, the conservative fixed-life assumption still holds. The capability is moving in one direction, but slowly, and the underwriting should move at the same pace.

Sources

Northrop Grumman SpaceLogistics, MEV-1 (Intelsat 901) and MEV-2 (Intelsat 10-02) mission records. NASA, OSAM-1 (On-orbit Servicing, Assembly, and Manufacturing 1) programme and 2024 cancellation notice. ESA, Clean Space and in-orbit servicing programmes (ClearSpace-1). Euroconsult, assessments of the in-orbit servicing and satellite life-extension market. DARPA, Robotic Servicing of Geosynchronous Satellites (RSGS) programme.